What is blockchain technology? A quick search of “blockchain” on Crunchbase, the startup and investing data base, yields 304 unique results. Blockstream, a startup focused on improving blockchain technology, has raised $76 million in funding. Chain, the leading blockchain platform for enterprises, has raised more than $43 million. Factom, Gem, Elliptic, Storj, Funderbeam, and Colu are just a few other examples of high-profile startups raising millions of dollars by employing blockchain technology.

But very few people can actually tell you what blockchain technology is. Most explanations that I’ve come across do a poor job of explaining the technology or its implications. How does it work? Why is it a big deal? How does it relate to bitcoin? This essay provides a simple and straightforward explanation of what blockchain technology is, so that later essays will be able to discuss the impact the technology will have on the startup and venture capital ecosystem.

Starting definitions

Many people first hear about blockchain technology in relation to bitcoin, so let’s start our explanation by differentiating between the two.

1. Bitcoin is a digital currency that allows transactions to take place between users directly, without the use of an intermediary; all transactions are verified by network nodes and recorded in a public distributed ledger called a blockchain.

The key takeaway from this definition is that bitcoin is just a currency that uses blockchain technology and has some unique characteristics. Bitcoins are units of exchange; the blockchain is where the bitcoin transactions are recorded and verified. So in a sense, blockchain technology is a broader, more fundamental concept than bitcoin.

2. A blockchain is a distributed database that maintains a continuously-growing list of records called “blocks”, which are secured from tampering and revision.

This definition is succinct, and might be nice if you already have an understanding of what a blockchain is, but it doesn’t do a good job of clearly explaining what the technology does. Because blockchain technology is such a broad concept, it’s difficult to conceptualize. In order to get a clear mental picture we’ll need work through an example, and because bitcoin is the most popular example of blockchain technology, that’s the one we’ll use. Please turn your attention to Figure 1.

Figure 1: The motivations behind bitcoin

To start, let’s try to understand the motivations behind the creation of a digital currency based on blockchain technology. According to the creator of bitcoin, Satoshi Nakamoto, the concept arose from a desire for a “purely peer-to-peer version of electronic cash.” Nakamoto wanted to eliminate the need for a trusted third party; he wanted to bypass the banks and corporations that stand behind conventional payment systems.

The goal of bitcoin, then, was to create a digital version of an in-person cash transaction. Exchanging physical currency doesn’t require a trusted intermediary. For those of you too young to have much familiarity with the rather dated idea of an in-person cash transaction, observe Figure 1.a.

Figure 1.a: Tom accidentally leaves his dirty protein-shake BlenderBottle lying around the house. The old milk and residual protein powder coat the BlenderBottle in a thick layer of mold, rendering it unusable and making a huge mess. Tom offers his younger brother, Joe, twenty dollars in cold, hard cash to clean the mess up for him. Strapping on a HAZMAT suit, Joe accepts the offer.

Here are the important points to note from this example: 1. Tom has cash; 2. Cash, which is mostly just cotton, is recognized as holding some assigned value; 3. Cash can be exchanged for other things that we value; 4. Tom gives cash to Joe for his service; 5. There was no intermediary during the transaction.

There are a number of positive characteristics to this form of transaction, but it is also limited in scope and stands to be improved in a number of ways. To see an example of the shortcomings of an in-person cash transaction, please turn to Figure 1.b.

Figure 1.b: Tom’s BlenderBottle has been irreparably damaged, with entire sections of the bottle having disintegrated under the fungal growth. He needs a new one, and is willing to exchange cash for it. However, the person who makes BlenderBottles is in Lehi, Utah, and Tom is not. He can’t simply hand cash to the person in exchange for the bottle. He wants the same benefits that came with his transaction with Joe (speed, reliability, independence from the third parties), but now he wants to be able to do it digitally.

We should now have a clear and basic understanding of the motivations behind bitcoin. The goal is a “peer-to-peer version of electronic cash”, a bypass of the current payment-processing middlemen, a digital equivalent of Tom directly giving Joe twenty bucks. These motivations lead us to blockchain technology.

Figure 2: An expanded definition of a blockchain

Recall from earlier that our definition of a blockchain was:

a distributed database that maintains a continuously-growing list of records called “blocks”, which are secured from tampering and revision

In other words, you can think about a blockchain as a list. It is an enormous, public list, and everyone that has access to the blockchain can see the list. As new submissions to the blockchain come in, they are bundled together to form a block, and each new block is connected to the previous one so that they form a sequential record.

The list is distributed in the sense that the data isn’t kept centrally. Every node (computer) in the network has a copy of the blockchain. No centralized, “official” copy exists, and no user’s copy of the blockchain is “trusted” more than anyone else’s.

The bitcoin blockchain, then, is a an enormous, public list of all of the bitcoin transactions that have taken place. It is public in the sense that any node connected to the network gets a copy of the blockchain and can verify that the listed transactions are legitimate. However, it is secure and private in the sense that information surrounding the transactions is encrypted.

Figure 3: Bitcoin transactions as an example to illustrate blockchain technology

Let’s assume that Tom has a number of bitcoins, and that the person in Lehi, Utah that is selling BlenderBottles is willing to accept bitcoin as a form of payment. Tom has software on his computer, a digital “bitcoin wallet”, that enables him to access the blockchain. In some ways, using this software to access the blockchain is similar to using a browser to access the web. However, the bitcoin wallet software keeps your identity hidden.

Tom submits a transaction to the blockchain proposing that some of the digital currency be moved from his wallet into the wallet of the person in Utah. This proposal propagates over the entire network of nodes (again, think computers that are using software to access the bitcoin blockchain). Specialized nodes called miners verify the transaction by checking the blockchain (the recorded list of all previous transactions) to ensure that Tom does in fact have the bitcoin that he is trying to send.

So far, in layman’s terms: Tom proposes a transaction to the network of computers (nodes). Specialized nodes (miners) check his proposal against the “copy” of the historical list (the blockchain) that they have, in order to make sure that Tom has enough bitcoin for his proposed transaction.

Once Tom’s transaction has been verified, miners bundle it together with other approved transactions to form a block.

“Bundle, that’s a nice tactile term. I’m assuming they use twine to bundle together these transactions?”

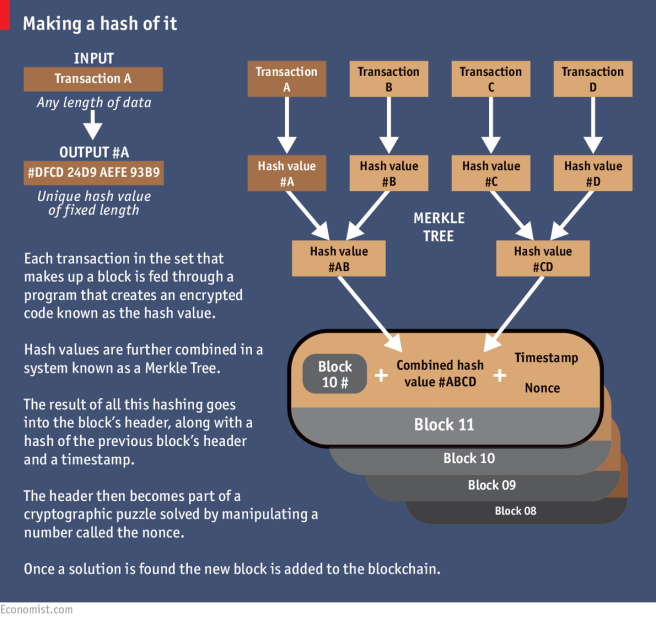

Not quite. When people talk about items being bundled together to form a block in the blockchain, they’re actually talking about encrypting the data. The data from Tom’s transaction is run through a cryptographic function which produces a string of digits called a hash value. This hash value serves as a unique identifier for the transaction data. It is relatively easy to go from the transaction data to the hash value, but it is impossible to go from the hash value to the transaction data.

The hash value for Tom’s verified transaction is then combined with the hash value of another verified transaction, creating a third hash value that represents both transactions. This process of boiling down all of the data into hash values is what is meant by “bundling”. Figure 3.a provides a visual representation of this explanation.

Figure 3.a:

So far, in layman’s terms: Tom proposes a transaction to the network of computers (nodes). Specialized nodes (miners) check his proposal against the “copy” of the historical list (the blockchain) that they have, in order to make sure that Tom has enough bitcoin for his proposed transaction. If he does, they take his transaction data and turn it into a string of digits (a hash value). This process is repeated over and over again to form a block (a set of encrypted data).

We haven’t yet discussed how a block is added to the end of the blockchain. In order to understand that part of the process, we have to elaborate on the specialized nodes called miners.

Miners are the nodes that work to verify proposed transaction and extend the blockchain by adding blocks. Any person that has access to the blockchain and is willing commit their time and computing power can be a miner. We’ve already noted that they verify transactions by comparing them to their copy of the blockchain and ensuring that participants have enough bitcoin for their proposals. We’ve also discussed how they encrypt the data by converting it into hash values. Once that process is completed and they’ve created a new block, miners compete with one another to add the block to the blockchain.

This competition takes the form of solving a complex mathematical puzzle that is generated using the hash value of the block. The puzzle can only be solved through trial and error, and miners churn through trillions and trillions of possible answers looking for the solution. Once the solution is found, the block is added to the blockchain and the updated list is distributed to all of the other nodes.

“Why would anyone go to all of the trouble of trying to verify these transactions and solve the mathematical problem?”

The mining node that solves the mathematical puzzle and adds the block to the blockchain is awarded a bitcoin payment as a prize.

“That seems like an overly complicated way of doing things.”

It may seem convoluted at first, but blockchain technology is really just a framework that combines different incentives to build trust in a decentralized system. Miners are incentivized to verify transactions because they may receive a bitcoin prize. The mathematical puzzle that is generated by the blockchain protocol is a way of ensuring that the miner receiving the prize is essentially random. Miners have to work hard to solve the puzzle, but all hard-working miners have essentially the same probability of solving the puzzle and winning the prize. This setup ensures that miners compete with each other, but in a way that strengthens the accountability of the blockchain record.

When a node receives an updated blockchain (i.e. when a miner sends out an updated list of transactions to other nodes), the node compares the new blockchain to the blockchain it already has on file to make sure that everything syncs up (except for the new block that has been added). If all of the historical records match, the node will replace its copy of the blockchain with the longer, updated version that it just received.

So far, in layman’s terms: Tom proposes a transaction to the network of computers (nodes). Specialized nodes (miners) check his proposal against the “copy” of the historical list (the blockchain) that they have, in order to make sure that Tom has enough bitcoin for his proposed transaction. If he does, they take his transaction data and turn it into a string of digits (a hash value). This process is repeated over and over again to form a block (a set of encrypted data). In order to add the block to the blockchain, miners compete to solve an arbitrary, complex, mathematical problem. The first to solve the puzzle wins a bitcoin prize, gets to add the block to the blockchain, and then distributes the updated blockchain to the other nodes.

Figure 4: What have we accomplished?

In what was essentially the equivalent of a digital in-person cash transaction, Tom paid the person in Utah for a new BlenderBottle. This is a significant accomplishment. Without relying on a centralized, trusted third party, without paying a premium, and without compromising any of his private information, Tom transmitted value to a distant location. The transfer of value was made in bitcoin, but the underlying system that made it possible was the blockchain.

“I’m still skeptical. Why is the blockchain a safer way to store data? Can’t someone just hack the blockchain in order to change the history of the list or give themselves more money?”

It can be a difficult idea to grasp, but the reason that the blockchain is safer is because it removes the central intermediary. Normally, criminal activity targets this trusted third party. Banks and corporations are the entities responsible for protecting our records and information, so they are often targeted by criminals. If an attacker is able to break through or fool the defenses of just one entity (a bank or corporation), they would be able to alter the information entrusted to the entity. However, because the blockchain is decentralized (remember that each participant has a copy of the information) an attacker would need to target at least 51% of all blockchain participants in order to successfully alter the data. While this type of attack is theoretically possible, it would be much more difficult than targeting a single entity and the effects of such an attack would probably prevent it from being profitable for the attacker. Unfortunately, a comprehensive analysis of attacks on the blockchain is outside the scope of this article. However, I think that we can safely say two things: 1. blockchain technology represents a powerful and revolutionary new tool for building trust and safety in a decentralized format; and 2. the technology is still young, and should be regarded with caution and optimism.

There are reasons to be excited and hopeful about the future of the system. Realizing that bitcoin is only one example of an application of blockchain technology, we can start to imagine other ways that the blockchain might be put to good use. It could theoretically improve music copyrighting, recording land ownership, voting, and other industries that rely on trusting a centralized (and often disorganized) source of data.

Blockchain technology will continue to spread, and as it does it will become more and more relevant to the startup and venture capital ecosystem. Understanding the technology in a fundamental way will allow us to have meaningful discussions on what exactly this coming change will look like.

One thought on “A Brief Introduction to Blockchain Technology”